Introductive remarks

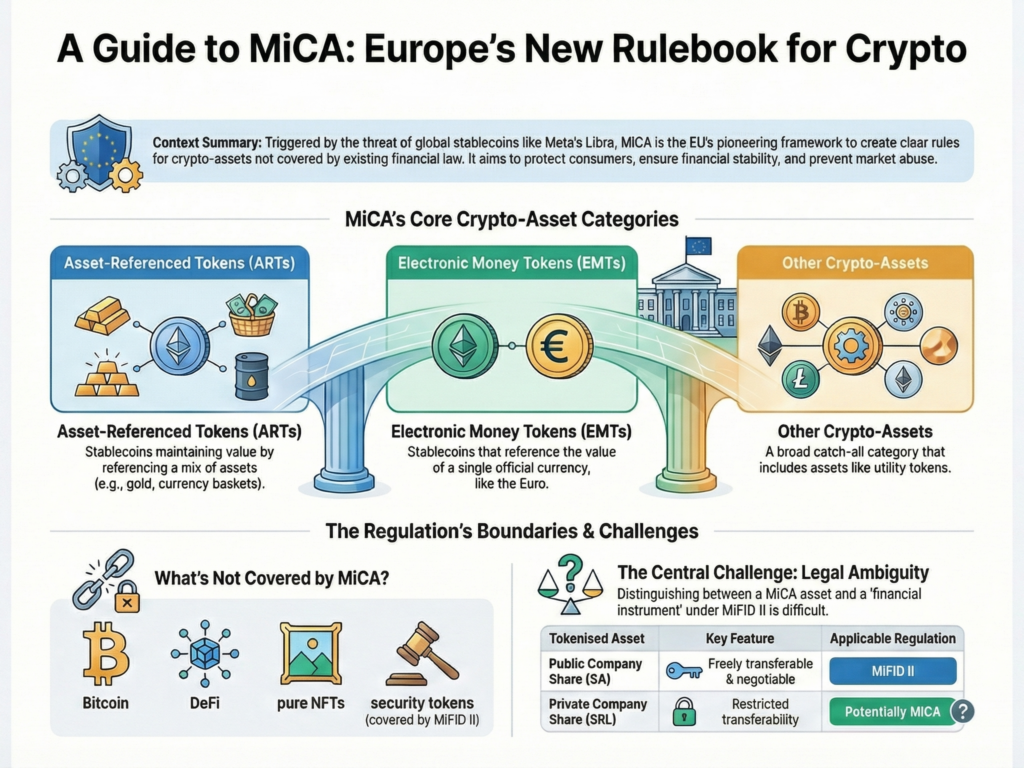

The Regulation on Markets in Crypto-Assets (MiCA) represents the European Union’s most ambitious legislative response to the evolving digital finance landscape. Triggered by the 2019 announcement of Meta’s Libra—a global stablecoin project that regulators viewed as a direct strike at monetary sovereignty and financial stability—MiCA was designed to prevent private, corporate-backed ecosystems from operating parallel to traditional financial infrastructure. Following extensive research by the ESMA and EBA, the framework was adopted in early 2023 and entered into force on 29 June 2023.

MiCA did not apply all at once; instead, it followed a phased implementation:

- 30 June 2024: Rules began applying to Asset-referenced Tokens (ARTs) and Electronic Money Tokens (EMTs).

- 30 December 2024: The remaining requirements, including those for Crypto-Asset Service Providers (CASPs) and other crypto-assets, become applicable.

- a grandfathering period allowed existing firms to operate the same way until July 1, 2026.

The national legislative framework in Romania for the implementation of Regulation (EU) 2023/1114 is currently in progress, with a draft law having been published for public consultation by the Ministry of Finance. At this stage, authorization applications under MiCA cannot yet be submitted, as they will only be accepted once the national implementing legislation enters into force and the competent authorities are formally designated. In the meantime, crypto-asset service providers operating in accordance with applicable law prior to 30 December 2024 may continue their activities during the transitional period until 1 July 2026 or until a decision on their authorization is issued, whichever occurs first.

The primary purpose of MiCA is to unify and clarify rules for the crypto-asset sector, ensuring transparency and protection for holders. It applies to any natural or legal person issuing, offering, or providing services related to crypto-assets within the EU. Under the framework, a crypto-asset is broadly defined as a digital representation of value or rights that can be transferred and stored electronically using distributed ledger technology (DLT).

After MICA, there are three regulatory categories of crypto assets:

- those classified as a financial instrument under MiFID II (or other regulated financial products),

- crypto-assets regulated by MiCA, and

- unregulated crypto-assets.

If you want to verify if your token is covered or not by MICA, you can get in contact with our team or acces our Assesment token Quiz. [1]

MiCA aims to fill the regulatory gaps for crypto-assets that are not already governed by existing financial law. It covers:

- Transparency & disclosure requirements for issuing and offering crypto-assets

- Authorization & supervision of CASPs, ART issuers, and EMT issuers

- Protection of crypto-asset holders and CASPs’s clients

- Measures against insider dealing, unlawful disclosure, and market manipulation

MiCA’s Crypto-Asset Classification

Under this umbrella, MiCA recognizes three core categories:

1. Asset-referenced Tokens (ARTs) – Stablecoins referencing multiple assets

A crypto-asset (not an EMT) that maintains stable value by referencing another value, right, or combination (e.g., gold, oil, fiat baskets).

2. Electronic Money Tokens (EMTs) – Stablecoins referencing a single official currency

A crypto-asset referencing the value of one official currency (e.g., USDT referencing the USD).

Example:

- If PayPal issues €-denominated e-money, PSD2 applies.

- If PayPal issues €-denominated e-money tokens, both PSD2 and MiCA apply.

3. Crypto-assets other than ARTs or EMTs – A broad category covering all other fungible and transferable assets with an identified issuer, such as Utility Tokens used for network fees or fan engagement

What Lies Outside MiCA?

Despite its broad reach, MiCA is technology-neutral but not limitless. Specifically, it does not cover:

- Fully decentralised systems or assets with no identifiable issuer (such as Bitcoin).

- DeFi applications and exchanges operating purely via smart contracts (currently considered a “grey area”).

- Central Bank Digital Currencies (CBDCs) and pure NFTs.

- Security Tokens: Assets classified as financial instruments fall under the MiFID II regime, which is mutually exclusive with MiCA.

However, distinguishing which regime applies is far from easy.

This distinction often rests on negotiability and transferability. For instance, tokenising a stock company share typically triggers MiFID II, whereas tokenising restricted limited liability parts might fall under MiCA. This ambiguity remains a challenge to the framework’s promise of total legal certainty.

Think of the crypto market as a vast, newly discovered territory. Before MiCA, it was the “Wild West”—innovative but chaotic, with no shared rules of the road. MiCA acts as the territory’s first comprehensive traffic code. It doesn’t try to pave every dirt path (decentralised systems), but for the major highways where businesses and public transport (stablecoins and service providers) operate, it sets the speed limits, safety standards, and licensing requirements to ensure everyone can travel without the system collapsing.

Coming Up Next in Our MiCA Deep Dive Series

This first article set the foundations: the political trigger behind MiCA, its architecture, scope, and the regulatory logic that shaped Europe’s approach to crypto-assets. In the next article, we will move from the why to the how and take a closer look at the core market participants regulated under MiCA.

Article 2 will focus on Crypto-Asset Service Providers (CASPs):

their authorization process, prudential obligations, governance rules, operational requirements, and the practical implications for exchanges, custodians, brokers, and trading platforms operating in or entering the EU market.

We will explore what it actually means to become a MiCA-compliant CASP, how regulators will supervise these entities, and what challenges and opportunities arise for both European and non-European players.

Stay tuned—the real operational heart of MiCA is just beginning.